[http://www.allaboutnews.com/img/invite_friend/envelope.gif]<http://[servername]/mmgw_invite_friend_form.php?username=%5binsertuser%5d> Send to a Friend <http://[servername]/mmgw_invite_friend_form.php?username=%5binsertuser%5d>

Follow Me On: [http://www.allaboutnews.com/images/social_icons/Facebook.jpg] <http://www.facebook.com/pages/Virginia-Beach-VA/Deanes-Group/195118023289> [http://www.allaboutnews.com/images/social_icons/Twitter.jpg] <http://www.twitter.com/deanesgroup> [http://www.allaboutnews.com/images/social_icons/LinkedIn.jpg] <http://www.linkedin.com/in/edeanes> [http://www.allaboutnews.com/images/social_icons/YouTube.jpg] [http://www.allaboutnews.com/images/social_icons/PlatPlus.jpg] <http://www.allaboutnews.com/platinumvideos/edeanes>

[http://members.platinumpromarketing.com/web/images/web/CC0C00_mmg_weekly_header.jpg]

[http://members.platinumpromarketing.com/members/web/16644_photo.jpg]

Edward F. W. Deanes

Home Mortgage Consultant

Wells Fargo Home Mortgage

Phone: (757) 418-2064

Fax:: (866) 935-0661

edward.deanes@wellsfargo.com<mailto:edward.deanes@wellsfargo.com>

www.deanesgroup.com

[http://members.platinumpromarketing.com/members/web/16644_logo.jpg]

In This Issue [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

Last Week in Review: The Fed faces a tough decision, but what could it mean for Bonds and home loan rates?

Forecast for the Week: This is a huge week, despite the limited number of reports due out... find out why.

View: Before you plan your next trip or a winter vacation, consider this surprising tip!

Last Week in Review [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

"I CAN NO LONGER STAND HERE WAITING FOR YOU TO DECIDE..." Those lyrics from the band Chicago's 1980's hit sum up the sentiments of many market analysts and traders after last week's back and forth statements from Fed officials about the possibility of another round of Quantitative Easing... otherwise known as "QE2".

As we stated last week, many analysts have been feeling that QE2 was very likely, if we continue to see weak economic reports. But comments made by a number of Fed officials throughout the week indicated that QE2 may still be up in the air. For example, Atlanta Federal Reserve President Dennis Lockhart stated, "there is growing sentiment that further accommodation through large asset purchases is coming... but at this point in time, it's not a foregone conclusion that we need to go there." Those comments were followed by other similar comments from other Fed officials, including Philadelphia Fed President Charles Plosser, who doesn't support any further Bond buying. Additionally, Boston Fed President Eric Rosengren said that monetary stimulus will depend on economic data, while Minnesota Fed President Narayana Kocherlakota says new asset buying would have a more muted impact than prior purchases. This would indicate that at least a few Fed members are hesitant about a big QE2 package.

On the flip side, however, New York Fed President William Dudley said on Friday that the Fed is almost certain to lend support through Quantitative Easing in order to ensure that a slowing economy does not fall further. He gave an example of how a $500 Billion purchase plan might impact interest rates, stating that it would have a similar impact to a Fed rate cut of .50 to .75%... and although this was just an example, the fact that he mentioned a specific number was not lost on Traders. Mr. Dudley went on to say that he feels a double dip recession is not an issue, but rather the focus is on how the economy can grow faster than its current pace.

Those comments are important because the markets figured that QE2 would be a lock, unless the Fed sees stronger-than-expected economic data before its November 3rd meeting... specifically, employment data. But last week the analysts and investors were faced with uncertainty around the issue and were left sifting through comments to try to predict what the Fed will do. And that uncertainty caused traders to shift money back out of Bonds at different times last week.

-----------------------

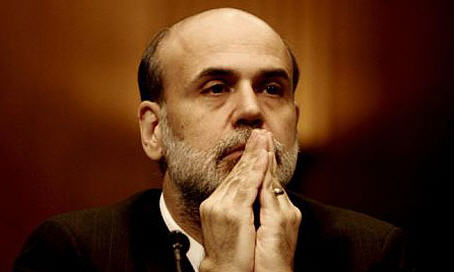

The Fed and Chairman Bernanke Face a Tough Decision with QE2

[http://www.mmgweekly.com/templates/mmgweekly/spe_chart/Top_Image_10_4_10.jpg]

But what would another round of Quantitative Easing mean to Bonds and home loan rates?

Let's break it down into four important aspects: (1) When would it happen? (2) How much money would it involve? (3) Why is this being contemplated? (4) And what does it mean to home loan rates?

First, as stated above, whether QE2 happens will be dependent upon the upcoming data releases. Many experts agree that if the Fed does make a move, it will most likely happen at the next Fed meeting, which is scheduled for November 3rd.

Second, the question of "how much" is still up in the air. As stated above, New York Fed President William Dudley gave an example of a $500 Billion purchase - but estimates are all over the board at this point, from $200 Billion to $2 Trillion. Yet the big question is whether QE2 will even do any good. Recently, former Fed Governor Larry Meyer felt that even $2 Trillion would hardly move the needle on GDP growth or reduce unemployment rates. In fact, he likens it to pushing on a string. Mr. Meyer's sentiments were also echoed last week by former Fed official Joe Gagnon, who estimated that the Fed is indeed likely to do at least $1 Trillion in additional QE, but that it would have little impact.

That brings us to the third question: Why even contemplate QE2? Think about this: a large round of QE2 would almost assuredly hurt the US Dollar. And by hurting the US Dollar, our exports become more affordable abroad, as well as making imports appear relatively more expensive. This helps large multi-national companies, which have a large influence on the economy, as well as the major Stock market indices. This could be the goal of the Fed. Ahh...but you can't outright say you are trying to weaken your currency. After all - haven't many members of Congress and the Administration been bashing China for currency manipulation? The US may be trying to do exactly what it has both denigrated and admonished other nations of doing.

In other words, even if QE2 didn't have a direct impact on the economy, the drop in currency value - which, if you've been paying attention to the Dollar-Euro relationship, has already been happening - would be very beneficial. But at what cost? While Stocks should benefit, Bonds may have a different reaction.

And that brings us to the heart of what you need to know: What would QE2 mean to Bonds and home loan rates?

If the Fed does go through with another round of Quantitative Easing, Bond prices should - initially - improve for two reasons. First, Bonds would likely improve due to the soft economic data causing QE2. Second, Bonds would improve simply because the announcement of QE2 would include large Bond purchases. The key word is "initially." That's because, even though Bonds would initially improve, the eventual softening of the Dollar, rising commodity prices, and rise in Stock prices could become a drag on Bonds, which would negatively impact home loan rates.

AS YOU CAN SEE FROM THIS DISCUSSION, THINGS AREN'T ALWAYS WHAT THEY SEEM. THE SAME IS TRUE FOR MANY FINANCIAL MATTERS. TAKE, FOR EXAMPLE, THE COST OF CHECKING YOUR LUGGAGE WHEN YOU FLY. CHECK OUT THE MORTGAGE MARKET GUIDE VIEW BELOW FOR SOME SURPRISING INFORMATION ON HOW YOU CAN SEND YOUR LUGGAGE FOR LESS!

Forecast for the Week [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

This week's economic calendar may be light in terms of the number of reports, but don't let that fool you for one second. The reports that are due out may have a huge impact not only on the economy this week, but also on decisions that will shape the economy for months to come.

We'll start off with an update on the health of the housing industry, with the Pending Home Sales report on Monday morning. After that, things start to heat up with the ADP National Employment Index on Wednesday and Initial Jobless Claims on Thursday. But the big enchilada comes on Friday, when the all-important Jobs Report will be released. This report includes official labor statistics on non-farm payrolls and the unemployment rate, as well as average hourly earnings and changes in the average work week.

These reports on employment are always important, but they take on even more significance in the current climate. That's because the question of whether the Fed will move forward with another round of Quantitative Easing as we've been discussing, depends heavily on the employment data that is released before the Fed's upcoming meeting on November 3rd. And since the release of the November Jobs Report on October data is due out November 5th - two days after the Fed meeting - this coming Friday's report is the last chance for the Fed members to see the official labor statistics before they meet to discuss QE2 and other financial policies.

Remember: Weak economic news normally causes money to flow out of Stocks and into Bonds, helping Bonds and home loan rates improve, while strong economic news normally has the opposite result. As you can see from the chart below, Mortgage Bonds experienced some volatility throughout last week. Overall, Bonds and home loan rates ended the week worse than where they began, despite the volatility.

With home loan rates still at historically good levels, homebuyers - and homeowners looking to refinance - still have a tremendous opportunity. But it won't last forever... which means now is a good time to act.

-----------------------

Chart: Fannie Mae 3.5% Mortgage Bond (Friday, October 1, 2010)

[http://members.platinumpromarketing.com/mmgw/charts/Weekly_Chart_10_4_10.jpg]

The Mortgage Market Guide View... [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

Save Money by Shipping Your Luggage

You may spend less by using a shipping company - rather than the airlines - to get your bags to your destination.

By Cameron Huddleston, Kiplinger.com<http://www.Kiplinger.com>

You may be able to save money by shipping your luggage rather than checking it in the next time you fly. The idea might sound absurd. But if you do the math - as Airfarewatchdog.com has done for you in this chart<http://www.airfarewatchdog.com/blog/4152043/shipping-vs-checking-which-would-you-rather-do/> - you'll see that it would cost you less in some cases to send your bags to your destination by FedEx, UPS or U.S. Postal Service ground shipping.

Passengers who have luggage that exceeds airlines' size and weight limits will score the biggest savings. They'll spend about $50 less by shipping one overweight suitcase than checking it in - and up to $200 by shipping two overweight bags.

Even if the cost is the same for shipping and checking bags, you get so much more from FedEx and UPS, says Airfarewatchdog.com founder George Hobica, who ships his luggage. They have better delivery records than the airlines, they provide tracking numbers so you can follow your shipment online and they let you insure items that the airlines don't, he says. Plus, you're more likely to get a refund from a shipping company than an airline if your luggage is damaged or lost.

Another benefit: You won't have to wait in long lines at the airport to check your bags. And if you have small children, you'll be a lot less stressed if you don't have to lug your kids and luggage from the parking lot to the terminal.

The key is to ship your luggage a few days BEFORE your flight so that it arrives at your destination when you do. If you're visiting a relative, the shipping logistics are easy. But if you're going to be staying in a hotel or condo, you should consider having the shipping company hold your items so you can pick them up. Otherwise, you might have to pay a fee to have the hotel or rental office hold your luggage until you arrive.

Reprinted with permission. All Contents c2010 The Kiplinger Washington Editors. www.kiplinger.com<http://www.Kiplinger.com>.

--------------------------

Economic Calendar for the Week of October 4-8, 2010

Remember, as a general rule, weaker than expected economic data is good for rates, while positive data causes rates to rise.

Economic Calendar for the Week of October 04 - October 08

Date

ET

Economic Report

For

Estimate

Actual

Prior

Impact

Mon. October 04

10:00

Pending Home Sales

Aug

1.0%

5.2%

Moderate

Tue. October 05

08:15

ISM Services Index

Sept

51.8

51.5

Moderate

Wed. October 06

08:15

ADP National Employment Report

Sept

18K

-10K

HIGH

Thu. October 07

01:00

Jobless Claims (Initial)

10/02

455K

453K

Moderate

Fri. October 08

08:30

Non-farm Payrolls

Sept

0

-54K

HIGH

Fri. October 08

08:30

Unemployment Rate

Sept

9.7%

9.6%

HIGH

Fri. October 08

08:30

Hourly Earnings

Sept

0.1%

0.3%

HIGH

Fri. October 08

08:30

Average Work Week

Sept

34.2

34.2

HIGH

The material contained in this newsletter has been prepared by an independent third-party provider. The content is provided for use by real estate, financial services and other professionals only and is not intended for consumer distribution. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, there is no guarantee it is not without errors.

As your trusted advisor, I am sending you the MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you.

Mortgage Market Guide, LLC is the copyright owner or licensee of the content and/or information in this email, unless otherwise indicated. Mortgage Market Guide, LLC does not grant to you a license to any content, features or materials in this email. You may not distribute, download, or save a copy of any of the content or screens except as otherwise provided in our Terms and Conditions of Membership, for any purpose.

[http://members.platinumpromarketing.com/web/images/web/ehlender.gif][http://members.platinumpromarketing.com/web/images/web/fdiclogo.gif]

[http://members.platinumpromarketing.com/tag.php?rs=%5bREPORTING_STRING%5d&urs=%5bCONTACT_STRING%5d]

Subscribe to:

Post Comments (Atom)

About Me

- Deanes Group

- My goal is to provide you with premium service. When you need an answer, we are here to help. I spend 90% of my time finding mortgages to fit my client's needs, qualifying buyers and contacting my clients for potential savings. My competent and professional staff handles all the dayto- day tasks. During regular business hours, please call my team, if they don't know the answer- they will find it! I am a licensed Loan Officer who has been in the mortgage industry for over 9 years. I am also a Certified Mortgage Planner which unlike a traditional loan officer; a mortgage planners role is to help you integrate the loan you select into your overall long and short-term financial and investment plans, to minimize taxes and interest expense and improve cash flow. I have a Real Estate License; not to practice real estate, but so I can better understand the market and look out for my client’s best interests. I am also a homeowner and real estate investor.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![http://members.platinumpromarketing.com/web/images/web/ehlender.gif][http://members.platinumpromarketing.com/web/images/web/fdiclogo.gif](http://members.platinumpromarketing.com/web/images/web/ehlender.gif][http://members.platinumpromarketing.com/web/images/web/fdiclogo.gif){kind=link}

No comments:

Post a Comment