[http://www.allaboutnews.com/img/invite_friend/envelope.gif]<http://%5bservername%5d/mmgw_invite_friend_form.php?username=%5binsertuser%5d> Send to a Friend <http://%5bservername%5d/mmgw_invite_friend_form.php?username=%5binsertuser%5d>

Follow Me On: [http://www.allaboutnews.com/images/social_icons/Facebook.jpg] <http://www.facebook.com/pages/Virginia-Beach-VA/Deanes-Group/195118023289> [http://www.allaboutnews.com/images/social_icons/Twitter.jpg] <http://www.twitter.com/deanesgroup> [http://www.allaboutnews.com/images/social_icons/LinkedIn.jpg] <http://www.linkedin.com/in/edeanes> [http://www.allaboutnews.com/images/social_icons/YouTube.jpg] [http://www.allaboutnews.com/images/social_icons/PlatPlus.jpg] <http://www.allaboutnews.com/platinumvideos/edeanes>

[http://members.platinumpromarketing.com/web/images/web/CC0C00_mmg_weekly_header.jpg]

[http://members.platinumpromarketing.com/members/web/16644_photo.jpg]

Edward F. W. Deanes

Home Mortgage Consultant

Wells Fargo Home Mortgage

Phone: (757) 418-2064

Fax:: (866) 935-0661

edward.deanes@wellsfargo.com<mailto:edward.deanes@wellsfargo.com>

www.deanesgroup.com

[http://members.platinumpromarketing.com/members/web/16644_logo.jpg]

In This Issue [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

Last Week in Review: Bonds may sink or swim on the value of the Chinese Yuan. Here's why.

Forecast for the Week: Why are the markets watching the Autumnal Equinox?

View: How to handle fundraisers and donation requests as the new school year starts.

Last Week in Review [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

"NOT ONLY CAN WATER FLOAT A BOAT - IT CAN SINK IT ALSO." Wise words, but you don't need to know that Chinese proverb to know that a knife can cut both ways. The same is true with the strong ties between the Chinese and US economies. For example, news came out last week that Chinese factories stepped up production in August, which helped ease concerns of a double-dip recession in US and, as a result, helped move Stocks higher earlier in the week. But additional news regarding China is also impacting the Bond market - and could impact home loan rates in the future, depending on how the events unfold.

Here's what's happening. There have been numerous accusations that China has kept their currency artificially low, in an effort to fuel their exports. Some American businesses remark that this is an unfair competitive advantage, and call for tariffs to be levied against Chinese goods. It would appear that a stronger Chinese Yuan would help to resolve this problem... but remember there can be some nasty unintended consequences, due to the relationship between Chinese currency and our Bond prices. The way that the Chinese keep their currency weak against the Dollar is by buying massive amounts of our Bonds, including Mortgage Backed Securities. And their heavy buying has helped keep home loan rates low. So strengthening the Yuan would require fewer purchases of our Bonds and Mortgage Backed Securities - and that would be negative for home loan rates.

To paraphrase the Chinese proverb above, the value of the Chinese Yuan may help determine whether Bonds sink or swim in the near future. That makes this a complicated situation... but you can count on me to continue to monitor it closely.

-----------------------

The Chinese Yuan May Help Bonds Sink or Swim

[http://www.mmgweekly.com/templates/mmgweekly/spe_chart/Top_Chart_9_20_10.jpg]

Bonds saw a nice rally earlier last week, due to speculation about the Fed making additional purchases of Bonds in the future. Last week, Goldman Sachs said the Fed may announce another $1 Trillion asset purchase at the November meeting. And while this is just speculation, many Bond traders bid prices higher on the chatter. Adding fuel to this story was an article in the Wall Street Journal, suggesting the same thing. On the other side of the debate, however, is Richmond Fed President Jeffrey Lacker, who stated that the US is far from needing more Bond purchasing by the Fed.

In other economic news, the Labor Department reported the inflation measuring Consumer Price Index (CPI) for August at 0.3%. That reading was just slightly above the 0.2% that was expected, but it was still a relatively tame reading. When stripping out volatile food and fuel, Core CPI was flat at 0.0%. This rather benign read on inflation allowed traders to breathe a sigh of relief and push Bonds higher. Prior to receiving the news, many traders were worried the CPI reading would be higher than expected. That's because the Producer Price Index (PPI) was reported the day before and showed wholesale inflation rose by 0.4% in August. That was above the 0.3% expected and the biggest gain in 5 months! Remember, inflation is the archenemy of Bonds and home loan rates, so any indication that inflation is increasing could cause home loan rates to worsen.

IT'S THAT TIME OF YEAR AGAIN! THE START OF THE NEW SCHOOL YEAR MEANS THE BEGINNING OF SCHOOL FUNDRAISERS AND DONATION REQUESTS. ALTHOUGH THE INTENTIONS ARE GOOD, THEY CAN BE TOUGH ON YOUR BUDGET. FOR TIPS ON HOW TO HANDLE ALL THOSE REQUESTS, CHECK OUT THE MORTGAGE MARKET GUIDE VIEW BELOW.

Forecast for the Week [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

The seasons are changing... but watching the calendar can also help us prepare for changes in the market, especially with Stocks now nearing a very important trading date. September 22 - which is the day of the Autumnal Equinox - has often marked an apex and turning point lower for market prices and events. Keep this in mind as we approach this date this Wednesday, especially with Stocks trading near tough technical resistance. If this trend holds, Stocks may head lower and help Bonds and home loan rates improve. But since traders are aware of this potential problem period for Stocks, an avoidance of the trend would likely have Stocks? players move into the Stock market with more gusto towards the end of next week, prompting a Bond sell off.

The Fed will hold their Federal Open Market Committee (FOMC) meeting next Tuesday - and always, the markets will be listening closely when the Fed's Monetary Policy and Rate Decision are announced.

Also on tap for next week are new reports on the health of the housing industry, beginning with Housing Starts and Building Permits for August on Tuesday. We'll also see reports on Existing Home Sales on Thursday and New Home Sales on Friday.

Thursday brings another round of Initial Jobless Claims. Last week, the Labor Department reported Initial Jobless Claims fell to 450,000, below estimates of 460,000 and the lowest reading in two months. While 450,000 claims are still a pretty high number, it is improved from recent readings.

Finally, we'll get a look at manufacturing on Friday with a new report on Durable Goods Orders for August. Durable Goods Orders are considered a leading indicator of manufacturing activity, and the market often moves on this report despite the volatility and large revisions that make it a less than perfect indicator.

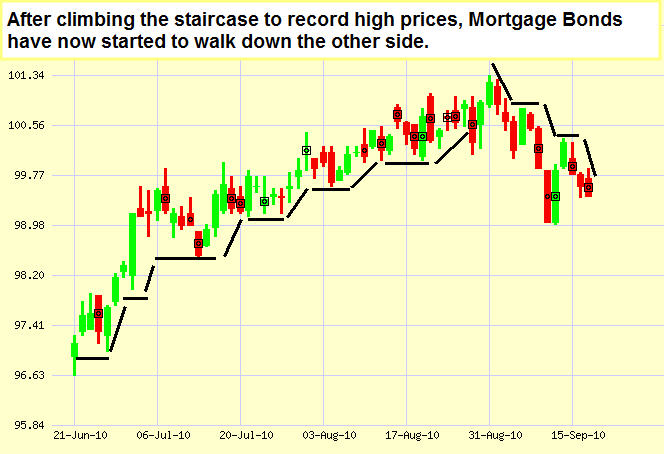

Remember: Weak economic news normally causes money to flow out of Stocks and into Bonds, helping Bonds and home loan rates improve, while strong economic news normally has the opposite result. As you can see from the chart below, Mortgage Bonds have started to step down after climbing to a record high at the end of August. Overall, Bonds and home loan rates ended the week worse than where they began.

The good news is home loan rates are still at historically great levels for homebuyers or homeowners looking to refinance... but that situation won't last forever.

-----------------------

Chart: Fannie Mae 3.5% Mortgage Bond (Friday, September 17, 2010)

[http://members.platinumpromarketing.com/mmgw/charts/Weekly_Chart_9_20_10.jpg]

The Mortgage Market Guide View... [http://www.mmgweekly.com/templates/images/weekly/sym_arrow.gif]

When Your Child's School Asks You to Give, Give, Give

Here's how to handle all those requests for classroom supplies, fundraiser contributions and more.

By Cameron Huddleston, Kiplinger.com<http://www.kiplinger.com>

Parents, I know you're feeling the pull on your purse strings from you children's schools. You're being asked to contribute supplies to your children's classrooms (not just pencils and paper, but even cleaning supplies). You're expected to donate money to help with the schools' fundraisers. You're getting notes from teachers each week about this field trip or that art project you have to pay for if your children want to participate.

I know because I'm a parent with one child in a public school and one child in a private preschool. As president of the parent committee at one of my children's schools and vice-president of the parent-teacher organization at the other, I also know how much the schools need financial support from parents. So how do you balance your desire to help with the reality of your own limited funds -- and avoid looking like a cheapskate if you can't open your wallet every time the school asks?

Even though this is your child and his school we're talking about, you have to approach this like you would any other financial situation. You have to...

Set a budget. If this is your child's first year in school, talk to his or teacher, parents with older children or members of the parent organization to get an idea of how much you'll be expected to spend on supplies, field trips, etc. or to contribute to fundraisers throughout the year. If your child is a returning student, you already have a pretty good idea. Once you have a dollar amount, it will be easier to figure out whether you can make room in your budget to help out your child's school. Our budget worksheet<http://www.kiplinger.com/tools/budget/> can help.

Prioritize. Of course the school, its parent committee and your child's teacher would love for you to donate every time they ask, but they also understand that not every parent can. So contribute only when it fits in your budget and when you feel like your contribution will have the most impact. That might mean skipping the chili-supper raffle in order to buy a coffee mug adorned with your child's art so his or her feelings don't get hurt.

Give your time. You might not be able to afford monetary contributions, but you can donate your time. Schools need volunteers to help in the classroom, cafeteria, you name it.

Reprinted with permission. All Contents c2010 The Kiplinger Washington Editors. www.kiplinger.com.<http://www.kiplinger.com>

--------------------------

Economic Calendar for the Week of September 20-24, 2010

Remember, as a general rule, weaker than expected economic data is good for rates, while positive data causes rates to rise.

Economic Calendar for the Week of September 20 - September 24

Date

ET

Economic Report

For

Estimate

Actual

Prior

Impact

Tue. September 21

08:30

Housing Starts

Aug

550K

546K

Moderate

Tue. September 21

08:30

Building Permits

Aug

555K

559K

Moderate

Tue. September 21

02:15

FOMC Meeting

9/21

0.25%

0.25%

HIGH

Wed. September 22

10:30

Crude Inventories

9/18

NA

-2.49M

Moderate

Thu. September 23

08:30

Jobless Claims (Initial)

9/18

NA

450K

Moderate

Thu. September 23

10:00

Existing Home Sales

Aug

4.11M

3.83M

Moderate

Thu. September 23

10:00

Index of Leading Econ Ind (LEI)

Aug

0.1%

0.1%

Moderate

Fri. September 24

08:30

Durable Goods Orders

Aug

-2.2%

0.3%

Moderate

Fri. September 24

10:00

New Home Sales

Aug

298K

276K

Moderate

[mmgwDisclosure]

The material contained in this newsletter has been prepared by an independent third-party provider. The content is provided for use by real estate, financial services and other professionals only and is not intended for consumer distribution. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, there is no guarantee it is not without errors.

As your trusted advisor, I am sending you the MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you.

Mortgage Market Guide, LLC is the copyright owner or licensee of the content and/or information in this email, unless otherwise indicated. Mortgage Market Guide, LLC does not grant to you a license to any content, features or materials in this email. You may not distribute, download, or save a copy of any of the content or screens except as otherwise provided in our Terms and Conditions of Membership, for any purpose.

[http://members.platinumpromarketing.com/web/images/web/ehlender.gif][http://members.platinumpromarketing.com/web/images/web/fdiclogo.gif]

[http://members.platinumpromarketing.com/tag.php?rs=%5bREPORTING_STRING%5d&urs=%5bCONTACT_STRING%5d]

Wednesday, September 22, 2010

Monday, September 20, 2010

Sept. 16, 2010 edition of Inside Mortgage Finance

According to the Sept. 16, 2010 edition of Inside Mortgage Finance, Wells Fargo was ranked as the top Purchase mortgage originator and the top Refinance Mortgage producer in the second quarter of 2010.

Wednesday, September 8, 2010

MMG Weekly: Special Holiday Article

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Another Business Booster from Edward F. W. Deanes - Meetings that Pack a Punch

| Follow Me On: | |||||||||||||||||

| |||||||||||||||||

| | |||||||||||||||||

| Meetings that Pack a Punch

Call me to discuss the presentations and seminars I can provide! | |||||||||||||||||

| |||||||||||||||||

© Copyright 2010. All About News, Inc.

FHA changes you need to know about!

FHA Implements Minimum Credit Scores

On September 3, 2010 Mortgagee Letter 10-29 was released. This mortgagee letter establishes minimum credit scoring requirements for all standard FHA programs* and is effective for case numbers assigned on or after October 4th, 2010.

Here are the 4 things you need to know about these changes:

1. Borrowers with a minimum credit score at or above 580 ARE eligible for maximum financing.

2. Borrowers with a minimum credit score between 500 and 579 ARE limited to a 90% LTV.

3. Borrowers with a minimum credit score of less than 500 are NOT eligible for FHA-insured mortgage financing.

4. Borrowers with a non-traditional credit history or insufficient credit are eligible for maximum financing BUT must meet the underwriting guidance in HUD 4155.1 4.C.3.

*Please note that these new requirements DO NOT apply to:Title I, Home Equity Conversion Mortgages; HOPE for Homeowners; Section 247; Section 248; Section 223(e), Section 238.

FHA MIP Changes Now Official

With the passing of H.R. 5981 and the resulting Public Law 111-229, FHA was given authority to change the amount charged to borrowers for both the Up Front and the Annual premiums. These changes as outlined in Mortgagee Letter 2010-28, are effective for all case numbers assigned on or after October 4th, 2010.

Here are the 6 things you need to know about these changes:

1. The Up Front premium is now 1.0 % for all standard FHA programs (purchase money mortgages, full credit-qualifying refinances, streamline refinances)

|

2. The Annual premium is now .90% for LTVs GREATER than 95% on 30 year loans

3. The Annual premium is now .85% for LTVs EQUAL to or LESS than 95% on 30 year loans

4. The Annual premium is now .25% for LTVs GREATER than 90% on 15 year loans

5. The Annual premium is now .00% for LTVs EQUAL to or LESS than 90% on 15 year loans

6. These premiums apply to purchases, regular refinances and streamlines

Please note that this new law also gives FHA the authority to raise the Annual premium at will up to 1.5% for LTVs at or below 95% and 1.55% for LTVs more than 95%.

Click here to read Mortgagee Letter 2010-28 in its entirety.

FHA Eliminates Unlimited CLTVs for Refinance Transactions

This update from Mortgagee Letter 2010-24 contains changes to the new maximum CLTV limits for refinance transactions, which will be effective for case numbers assigned on or after September 7, 2010.

The combined amount of the FHA-insured first mortgage and any subordinate lien may not exceed the applicable FHA LTV AND the geographical maximum mortgage amount (does not apply to streamline refinance transactions).

Here are the 4 Maximum CLTVs for Refinance Transactions that you need to know about:

1. Rate and Term (or No Cash Out) Refinances = 97.75%

2. Refinances for Borrowers in Negative Equity Positions* = 115%

3. FHA-to-FHA Streamline Refinances With or Without Appraisals = 125%

4. Cash-out Refinances = 85%

* This refinance option is only available through December 31, 2012. Read Mortgagee Letter 2010-23 for more information.

For more information, read Mortgagee Letter 2010-24 in its entirety.

Thank you,

Edward Deanes

This information is accurate as of the date posted and is subject to change without notice. All of the views and comments are mine and do not represent Wells Fargo.

Subscribe to:

Posts (Atom)

About Me

- Deanes Group

- My goal is to provide you with premium service. When you need an answer, we are here to help. I spend 90% of my time finding mortgages to fit my client's needs, qualifying buyers and contacting my clients for potential savings. My competent and professional staff handles all the dayto- day tasks. During regular business hours, please call my team, if they don't know the answer- they will find it! I am a licensed Loan Officer who has been in the mortgage industry for over 9 years. I am also a Certified Mortgage Planner which unlike a traditional loan officer; a mortgage planners role is to help you integrate the loan you select into your overall long and short-term financial and investment plans, to minimize taxes and interest expense and improve cash flow. I have a Real Estate License; not to practice real estate, but so I can better understand the market and look out for my client’s best interests. I am also a homeowner and real estate investor.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![http://members.platinumpromarketing.com/web/images/web/ehlender.gif][http://members.platinumpromarketing.com/web/images/web/fdiclogo.gif](http://members.platinumpromarketing.com/web/images/web/ehlender.gif][http://members.platinumpromarketing.com/web/images/web/fdiclogo.gif){kind=link}